Article

Implementing Regime-Switching Models for Macroeconomic Stress Testing

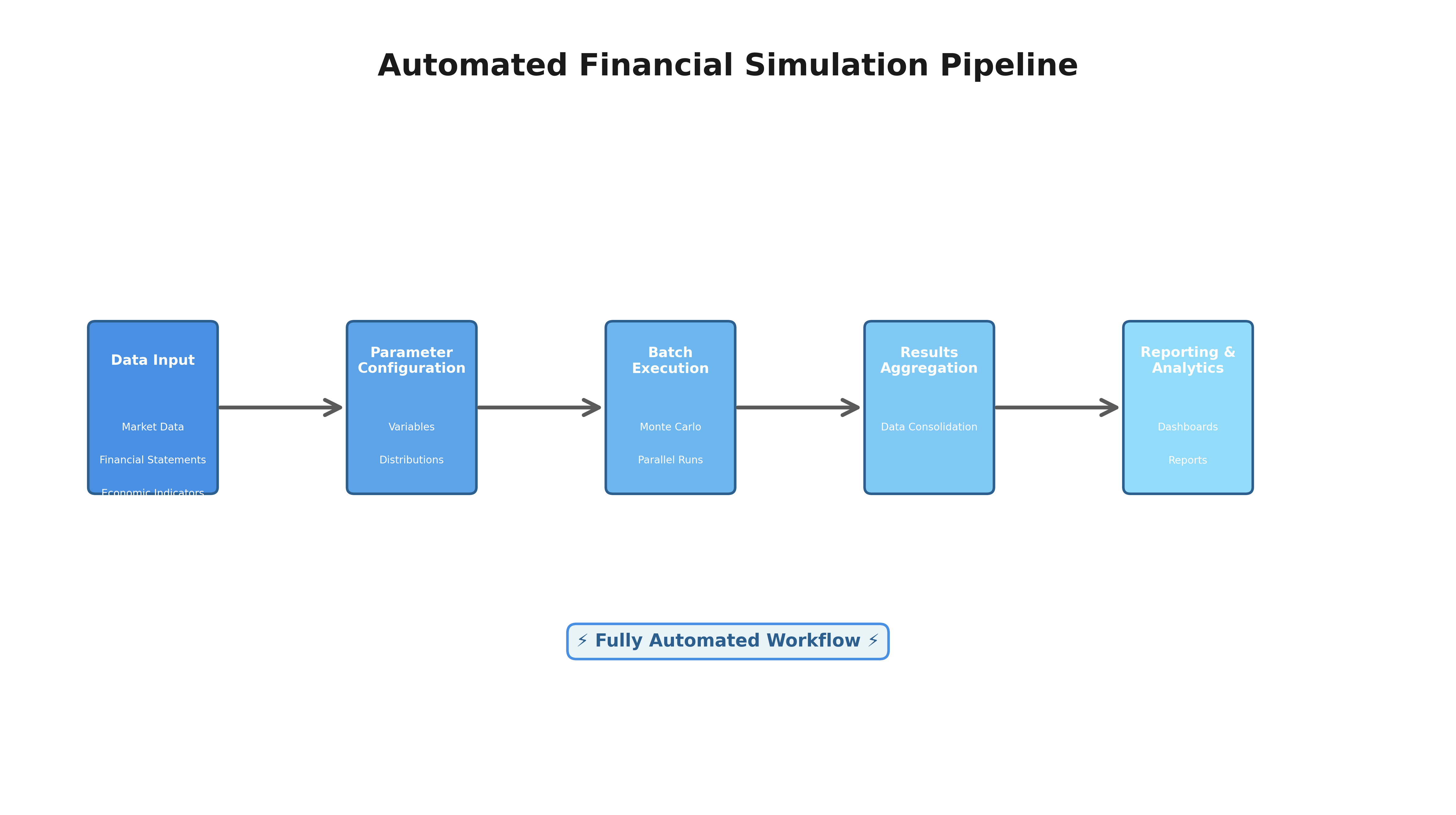

Regime-switching models capture structural breaks in financial markets by allowing statistical properties to vary across latent economic states. This article covers practical implementation of Hamilton Markov-Switching models in Python, forward simulation for stress testing, and integration with regulatory frameworks such as DFAST and CCAR.

By Jeff

23 views